Data insights now available in Mortgage MarketSmart show refinance-driven growth amid rising loan sizes

DES MOINES, Iowa /Florida Newswire – National News/ — iEmergent, a forecasting and advisory services firm for the financial services, mortgage and real estate industries, has released its analysis of 2025 Home Mortgage Disclosure Act (HMDA) data in Mortgage MarketSmart. Presented by iEmergent CEO Laird Nossuli, the findings point to a market that is regaining momentum after a prolonged downturn, with total volume increasing in 2025. That recovery, however, is uneven. Growth is being driven by refinancing activity and larger loan balances, while competitive gains remain concentrated among a relatively small group of lenders.

Top takeaways from 2025 HMDA data:

1. Refinance activity drove a disproportionate share of volume growth.

U.S. lenders originated approximately 6.75 million loans totaling $2.12 trillion in 2025, up from $1.82 trillion in 2024. Refinances accounted for a disproportionate share of that growth, rising to $610.4 billion and representing 29% of total lending volume, compared to 22% the prior year. This shift indicates that recent volume gains are being fueled more by rate-driven activity than by underlying purchase demand.

2. IMBs extended their lead in both share and growth capture.

Independent mortgage banks (IMBs) increased their share of originations to 57.8% in 2025, up from 55.8% in 2024, and accounted for 61.9% of total lending volume. Notably, they captured $193 billion of the market’s $303 billion year-over-year growth, far outpacing depository institutions. IMBs also dominated lender rankings, representing 18 of the top 25 institutions by both loan count and dollar volume.

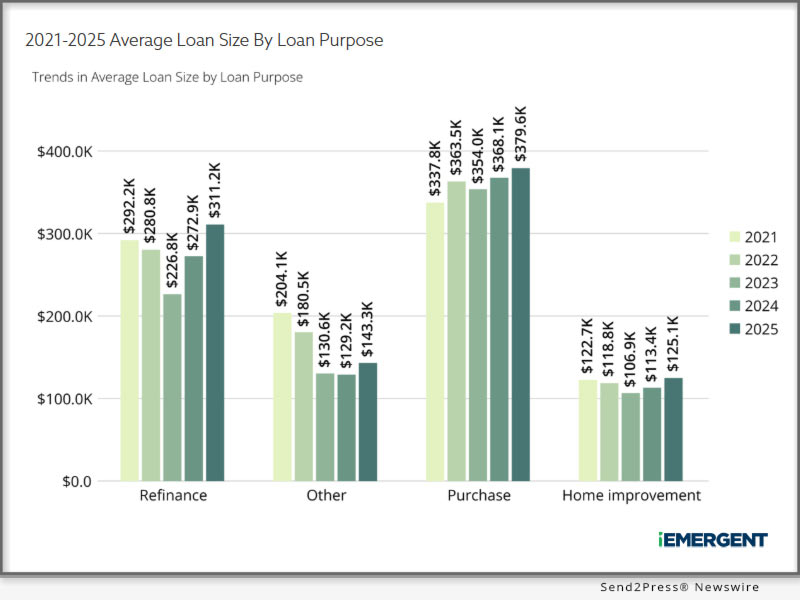

3. Rising loan sizes continue to pressure affordability.

Average loan sizes increased across both purchase and refinance segments, with purchase loans rising to $379,600 (from $368,100) and refinance loans to $311,200 (from $272,900). These increases align with persistent inventory constraints and elevated home prices, which are pushing borrowers toward higher balances and further limiting access for more price-sensitive buyers.

4. Denial rates edged down, but elevated fallout points to ongoing borrower friction.

While denial rates declined modestly, overall application fallout remained high. Approximately 40% of applications from non-Hispanic White borrowers did not result in funded loans, while fallout exceeded 50% for Black, Native American/Alaskan and Pacific Islander applicants. Increased withdrawals and incomplete applications suggest that affordability constraints and valuation challenges are continuing to disrupt borrower progression through the origination process.

5. Market concentration remains high, with production concentrated among a small group of lenders.

The top five lenders accounted for just over 20% of both loan count and total volume in 2025. More broadly, only 47 lenders-roughly 1% of all institutions-originated half of total mortgage volume. This concentration underscores a competitive environment in which scale and operational efficiency are increasingly determining market share outcomes.

6. Loan purpose mix varies significantly by geography, reinforcing the need for localized strategy.

Purchase-driven markets in the Sun Belt, such as Houston (71% purchase) and Austin (68% purchase), stand in contrast to coastal markets like Los Angeles (40% refinance) and San Diego (38% refinance). These differences highlight the importance of market-specific strategy, as performance in purchase-heavy regions depends more on execution and affordability positioning than on cyclical refinance opportunities.

“2025 HMDA data shows a market that is improving, but not uniformly,” said Nossuli. “Growth is being driven by specific products, borrower segments and geographies, while competitive gains are concentrated among lenders with the scale and strategy to capture them. Understanding where those opportunities exist is critical for lenders planning their next phase of growth.”

Lenders can now benchmark performance and identify growth opportunities

The integration of 2025 HMDA data into Mortgage MarketSmart allows lenders to benchmark their performance against peers across categories such as:

* Purchase and refi loan volume (units and dollars)

* Borrower race and ethnicity

* Loan type and size

* Borrower income levels

* Denial reasons by demographic group

With side-by-side comparisons of HMDA data, historical trends and forward-looking forecasts, Mortgage MarketSmart empowers lenders to identify gaps, meet Community Reinvestment Act (CRA) obligations and reach underserved markets.

To explore 2025 HMDA insights in Mortgage MarketSmart, request a demo at https://www.iemergent.com.

About iEmergent

Founded in 2000, iEmergent provides mortgage lending forecasts and analytics to the lending, housing and real estate industries. The company offers an extensive variety of forecast and market intelligence products, including Mortgage MarketSmart, a visualization tool that helps lenders quantify how mortgage markets will change. For more information, visit https://www.iemergent.com/.

Learn More: https://www.iemergent.com

This version of news story was published on and is Copr. © 2026 Florida Newswire® (FloridaNewswire.com) – part of the Neotrope® News Network, USA – all rights reserved.

Information is believed accurate but is not guaranteed. For questions about the above news, contact the company/org/person noted in the text and NOT this website.

NEWS SOURCE: iEmergent. Story was sourced from a press release issued by Send2Press® and used with permission. View the original story at: https://www.send2press.com/wire/iemergent-releases-2025-hmda-insights-volume-rebounds-but-the-mortgage-market-grows-more-concentrated/

{kind=link}